In 1989, Joshua Boger and Kevin Kinsella founded Vertex Pharmaceuticals in Cambridge, Massachusetts to transform the treatment of serious diseases. They listed on the NASDAQ stock exchange in 1991 as a public company.

Vertex uses biotechnology to develop its medicines. That is, living organisms undergo extraction or manipulation to make the drugs . They focus on innovation that creates transformative medicines for people with serious diseases. Their products include multiple medicines that treat the underlying cause of cystic fibrosis (CF) – a rare, life-threatening disease. They also have multiple ongoing research and development of CF drugs. Again, they have multiple projects in their pipeline for sicknesses such as sickle cell disease, beta-thalassemia, APOL1-mediated kidney disease, pain, type 1 diabetes, alpha-1 antitrypsin deficiency, and Duchenne muscular dystrophy.

In January 2014, Vertex moved its headquarters to Boston, Massachusetts. They employ 3,900 people as of 2019.

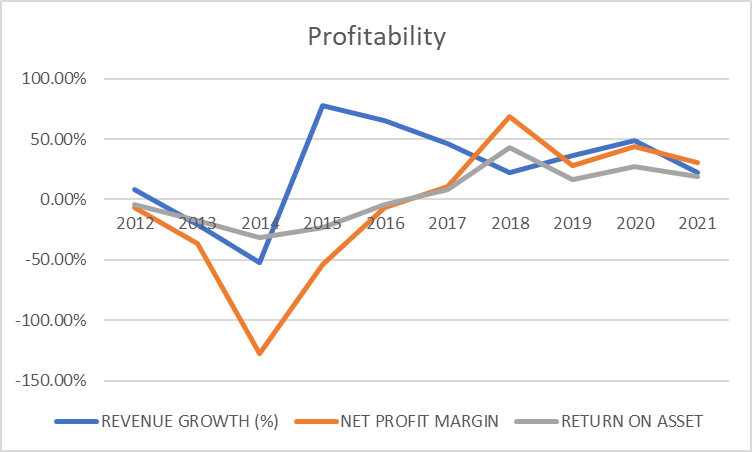

Profitability

Vertex posted $1.5B revenue in 2012. By 2021, its revenue jumped to $7.5B, representing a compound growth rate (CAGR) of 17.38%. However, there were hiccups along the way. They suffered revenue declines in 2013 and 2014 due to decreases in royalty income. Vertex returned to positive revenue growth in 2015 after introducing a new drug called Orkambi.

From 2012 to 2016, Vertex posted losses due to poor revenue performance. They returned to profitability in 2017 because of the rapid growth of Orkambi sales revenue. This is reflected in high net profit margins from 2017 to 2021.

Vertex’s return on asset (ROA) performance mirrored its net profit margin performance. ROA was negative from 2012 to 2016. Conversely, ROA was positive from 2017 to 2021 hitting a peak of 42.8 in 2018.

Capital Structure

Vertex uses mostly equity to fund its assets. Most loans are structured as convertible notes. Thus, lenders can convert the debt to shares when due for collection. For instance, in 2013 a creditor redeemed a $400M note in shares.

In 2014, Vertex secured a loan of up to $500M and received $300M of the amount in the same year. This altered Vertex’s capital structure metrics. The debt was paid off in 2017.

Market Analysis

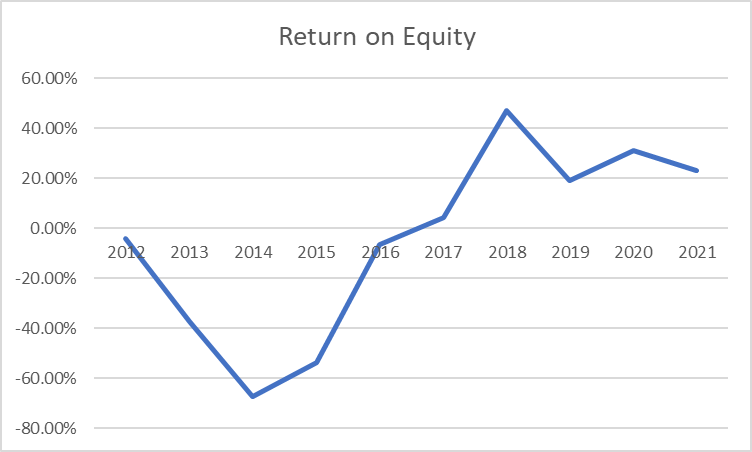

Vertex did not consistently generate profit with shareholders’ funds. As a result, shareholders’ funds were degraded from 2012 to 2016 due to losses. Starting in 2017, the company returned some value to shareholders. Therefore, Vertex managed average basic earnings per share (EPS) of $2.50 over the 10 years.

The poor use of shareholders’ funds is more evident when you look at the return on equity (ROE). The average ROE was -4.33% over the 10 years.

SWOT Analysis

Research and development (R&D) was a major strength of Vertex. They also maintained sufficient short-term assets to fulfill their short-term commitments. Again, the management implemented a good debt management strategy. As a result, the company did not rely on debt.

Conversely, the management did not display strong control over the company revenue. They sold off the royalty rights for their largest source of revenue when there was no replacement at hand. It took the company two years to recover. Also, the company does not have multiple major revenue-generating drugs.

Vertex can use its strong R&D to develop more drugs to diversify revenue streams.

Recommendations to Shareholders

I would recommend for investors buy and hold Vertex stocks. Despite initially posting losses, Vertex has shown strong revenue growth subsequently. The growth is expected to continue as Vertex expands its drugs into new markets and develops new products.

YOUR BIASES CAN KILL YOU

YOUR BIASES CAN KILL YOU