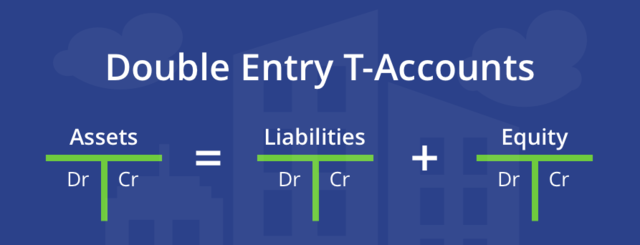

Recording accounting transactions is a fundamental aspect of the accounting process, crucial for maintaining accurate financial records and facilitating effective financial management. This process involves systematically documenting all financial activities and events that impact an organization’s financial position. The double-entry accounting system is commonly used, where each transaction affects at least two accounts—debiting one account and crediting another. The process begins with identifying and recognizing all relevant financial transactions. These transactions can include sales, purchases, expenses, investments, borrowings, repayments, and other financial activities.

Supporting documents, known as source documents, provide evidence of the transactions. Examples of source documents include invoices, receipts, purchase orders, bank statements, and contracts. These documents serve as a basis for recording transactions in the accounting system. Before recording a transaction, accountants analyze its impact on the organization’s financial position. They determine which accounts or elements are affected and the nature of those effects, such as increases or decreases in assets, liabilities, equity, revenue, or expenses. The double-entry accounting system requires recording each transaction with at least one debit and one credit. Debits and credits must always balance, ensuring that the accounting equation (Assets = Liabilities + Equity) remains in equilibrium. Debits and credits are recorded in specific accounts based on accounting principles.

Increase in assets: Debit, Decrease in assets: Credit, Increase in liabilities: Credit, Decrease in liabilities: Debit, Increase in equity: Credit, Decrease in equity: Debit, Increase in Revenue: Credit, Decrease in Revenue: Debit, Increase in Expenses: Debit, Decrease in Expenses: Credit.

Journal entries are the initial recordings of transactions in chronological order. Each journal entry includes the date, accounts affected, a brief description of the transaction, and the debit and credit amounts. Entries are made in the general journal. After journal entries are made, the amounts are posted to corresponding ledger accounts. The ledger organizes and summarizes the balances of individual accounts. Accounts include assets, liabilities, equity, revenue, and expense accounts. A trial balance is prepared to verify the accuracy of the recorded transactions. It lists all the accounts with their respective debit and credit balances. If the trial balance is in balance (total debits equal total credits), it suggests that the recording process is accurate.

Adjusting entries are made at the end of an accounting period to account for items like accrued expenses, prepaid income, and depreciation. These entries ensure that financial statements reflect the organization’s financial position accurately. Financial statements, including the income statement, balance sheet, and statement of cash flows, are prepared based on the recorded transactions. These statements provide a comprehensive view of the organization’s financial performance and position.

Keeping accurate and organized financial records is a crucial aspect of managing a business or personal finances. Proper financial record-keeping provides a clear and detailed picture of the financial health of an entity and supports various functions, including budgeting, tax compliance, decision-making, and financial planning. In summary, keeping financial records is a disciplined and strategic practice that contributes to financial stability, compliance, and effective decision-making. It is an integral part of sound financial management for both businesses and individuals.

Important terms, concepts, notes, formulae and structures so far in CFA (corporate financial accounting

Important terms, concepts, notes, formulae and structures so far in CFA (corporate financial accounting