The entity idea is a fundamental notion in accounting that establishes the business as a separate entity from its owners or shareholders. The entity idea aids in the establishment of any business’s accounting structure, determining how financial transactions are recorded and reported. In this blog post, we will look at the entity idea and its role in accounting.

What exactly is the Entity Concept?

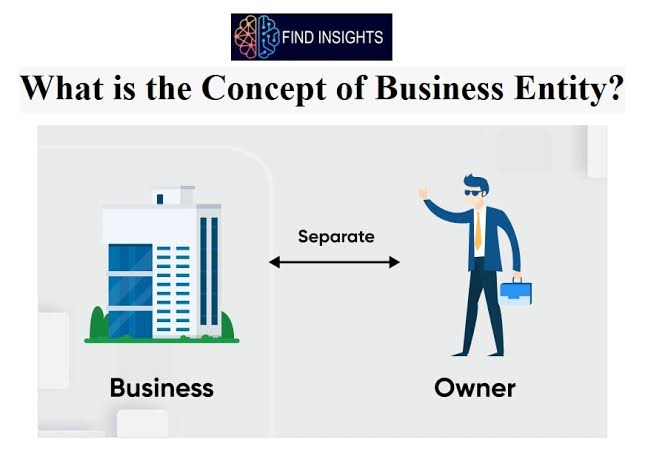

The entity notion indicates that a firm is distinct from its owners or shareholders, requiring its financial actions to be reported separately. This means that any company transactions must be recorded separately from those of the owners, and vice versa. Essentially, the entity notion distinguishes between personal funds and corporate finances.

The entity idea is crucial because it allows for the correct and transparent recording of financial transactions, which makes tracking and analyzing a company’s performance easier. It also aids in the enforcement of accounting standards such as the Generally Accepted Accounting Principles (GAAP).

Entity Classes

Corporations, partnerships, sole proprietorships, and non-profit organizations are all examples of entities. Regardless of their legal structure, the entity notion applies to all sorts of businesses. The concept remains the same: the business’s financial operations must be kept separate from those of the owners or shareholders.

Exemplifications of the Entity Concept in Action

Consider the following examples to better grasp the entity concept:

Example 1: A sole proprietorship is a form of firm in which the owner and operator are the same person. The owner’s personal money are kept separate from the corporate finances in this situation. If the owner uses personal funds to buy new business equipment, the transaction must be documented separately as a business expense.

Example 2: A corporation is a legal entity distinct from its owners or shareholders. When a corporation offers stock, the shareholders own a portion of the company but have no direct influence over its day-to-day operations. The financial transactions of the corporation must be recorded separately from those of the shareholders.

Example 3: A partnership is a business that is owned by two or more people. The partnership’s financial transactions must be kept separate from each partner’s personal finances. If a partnership partner withdraws cash for personal use, the transaction must be documented separately as a distribution to the partner.

The Benefits of the Entity Concept

The entity notion has various benefits, including:

Improved financial reporting accuracy and transparency: By separating personal finances from corporate finances, the entity idea makes it easier to accurately track and assess a company’s financial performance.

Legal protection: The entity idea gives legal protection to the business’s owners. In the event of a litigation or bankruptcy, the assets of the company are separate from the owners’ personal assets.

Easier compliance with accounting standards: The entity concept is a key accounting principle that must be followed to achieve compliance with accounting standards such as GAAP.

Conclusion

The entity idea is a fundamental principle in accounting that distinguishes between personal and commercial accounts. The entity concept ensures accurate and transparent financial reporting by isolating the financial transactions of the business from those of the owners or shareholders. This principle applies to all sorts of enterprises, from single proprietorships to corporations, and is essential for accounting standards compliance. Anyone involved in accounting, finance, or business operations must understand the entity idea.

A GLIMPSE INTO THE ENTREPRENEURIAL JOURNEY OF CEDRIC FILET AND THE RISE OF ALDELIA LTD.

A GLIMPSE INTO THE ENTREPRENEURIAL JOURNEY OF CEDRIC FILET AND THE RISE OF ALDELIA LTD.