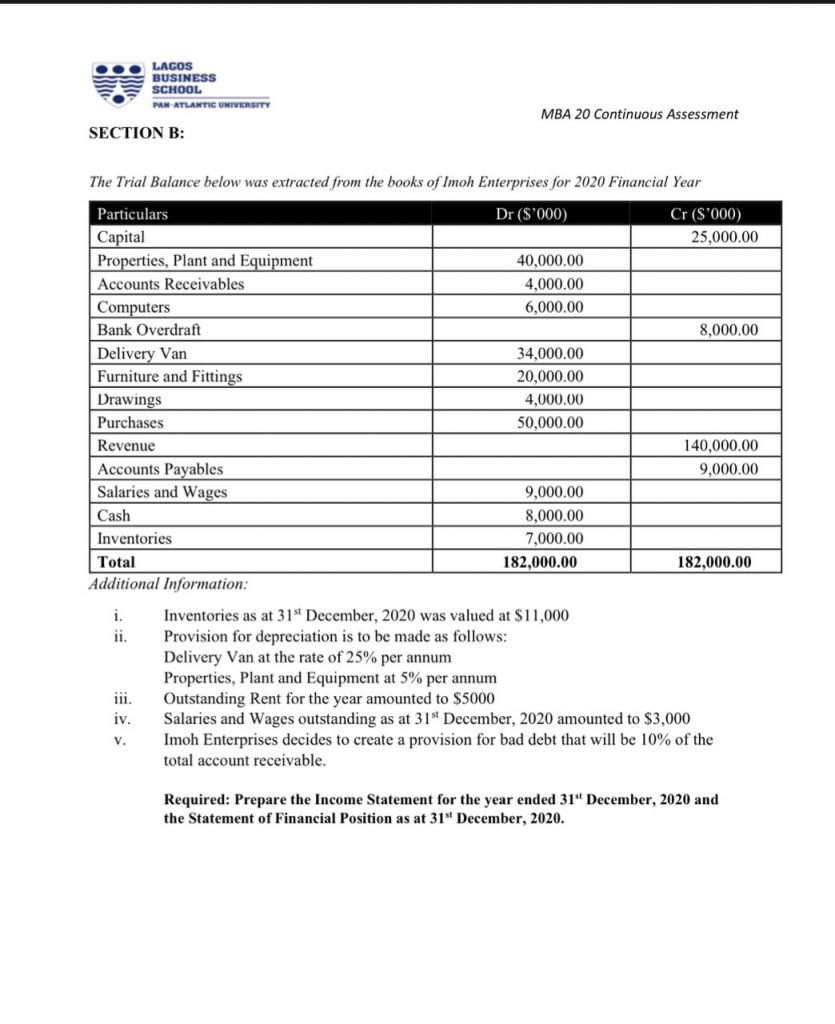

So, i had CFA test today. It was was adjusting trial balance creating income statement and financial statement them by choice Trial Balance.

I wonder how I could enlighten everyone with the questions.

I had my own personal answers. Well what can I really say I tried. I think its good enough.

| Books of imoh Enterprise | for 2020 year ended 31st financial year. | |||||||||||

| Income statement | ||||||||||||

| NOTE 2 | ||||||||||||

| DR | CASH | CR | Provision for Depreciation | |||||||||

| opening inventory | 7,000 | Description | Debit($) | Description | ||||||||

| Purchases | 50,000.00 | bal c/d | 10,500 | DV Depreciation expense | ||||||||

| COGAS | 57,000.00 | PPE Depreciation expense | ||||||||||

| Closing Inventory | (11,000) | 10,500 | ||||||||||

| COG | 46,000.00 | |||||||||||

| NOTE 4 | PPE Depreciation expense | |||||||||||

| DV Depreciation expense | Description | Debit($) | Description | Credit($) | ||||||||

| Description | Debit($) | Description | Credit($) | 2,000 | P or L | 2,000 | ||||||

| Provision for Depreciation | P or L | |||||||||||

| Bal/bd | 2,000 | |||||||||||

| Rent | NOTE 6 | Accrued Rent | ||||||||||

| Description | Debit($) | Description | Credit($) | Description | Debit($) | Description | Credit($) | |||||

| Accrued Rent | 5,000 | P or L | 5,000 | bal c/d | Rent | |||||||

| NOTE 8 | accrued Salaries | |||||||||||

| Salaries and wages | Description | Debit($) | Description | Credit($) | ||||||||

| Description | Debit($) | Description | Credit($) | bal c/d | Salaries and wages | |||||||

| bal b/d | 9,000 | P or L | ||||||||||

| accrued Salaries | 3,000 | |||||||||||

| 12,000 | 12,000 | |||||||||||

| Provision for bad debt | NOTE 10 | Account Receivables | ||||||||||

| Description | Debit($) | Description | Credit($) | Description | Debit($) | Description | Credit($) | |||||

| P or L | 400 | Account Receivables | 400 | bal b/d | 4,000 | bal c/d | 4,000 | |||||

| Provision for bad debt | 0 | |||||||||||

| 4,000 | 4,000 | |||||||||||

| Note 11 | Operating Expense | |||||||||||

| Salaries and Wages | 12,000 | |||||||||||

| DV Depreciation expense | 8,500 | |||||||||||

| PPE Depreciation expense | 2,000 | |||||||||||

| Rent | 5,000 | |||||||||||

| Provision for bad debt | 400 | |||||||||||

| 27,900 | ||||||||||||

| IMOH ENTERPRISES | ||||||||||||

| STATEMENT OF FINANCIAL POSITION AS AT 31ST DECEMBER 2020. | ||||||||||||

| Assets | Notes | $ | ||||||||||

| Non Current Asset | ||||||||||||

| Properties, Plant and Equipment | 2,000 | |||||||||||

| Delivery Van | 8,500 | |||||||||||

| Furniture and Fittings | 20,000 | |||||||||||

| Current Assets | ||||||||||||

| Computers | 6,000 | |||||||||||

| Accounts Receivables | 4,400 | |||||||||||

| Cash | 8,000 | |||||||||||

| Inventories | 11,000 | |||||||||||

| 29,400 | ||||||||||||

| Liabilities | ||||||||||||

| Bank Overdraft | 8,000 | |||||||||||

| Accounts Payables | 9,000 | |||||||||||

| Provision for Depreciation | 10,500 | |||||||||||

| Accrued Rent | 5,000 | |||||||||||

| accrued Salaries | 3,000 | |||||||||||

| 35,500 | ||||||||||||

| owners Equity | ||||||||||||

| Capital | 25,000 | |||||||||||

| Drawings | (4,000) | |||||||||||

| 21,000 | ||||||||||||

| 85,900 | ||||||||||||

| Adjusted Trial Balance | ||||||||||||

| Particulars | Dr($’000) | Cr($’000) | ||||||||||

| Capital | 25,000 | |||||||||||

| Properties, Plant and Equipment | 40,000 | |||||||||||

| Accounts Receivables | 4,400 | |||||||||||

| Computers | 6,000 | |||||||||||

| Bank Overdraft | 8,000 | |||||||||||

| Delivery Van | 34,000 | |||||||||||

| Furniture and Fittings | 20,000 | |||||||||||

| Drawings | 4,000 | |||||||||||

| Purchases | 50,000 | |||||||||||

| Revenue | 140,000 | |||||||||||

| Accounts Payables | 9,000 | |||||||||||

| Salaries and Wages | 12,000 | |||||||||||

| Cash | 8,000 | |||||||||||

| Inventories | 7,000 | |||||||||||

| Provision for Depreciation | 10,500 | |||||||||||

| DV Depreciation expense | 8,500 | |||||||||||

| PPE Depreciation expense | 2,000 | |||||||||||

| Rent | 5,000 | |||||||||||

| Accrued Rent | 5,000 | |||||||||||

| accrued Salaries | 3,000 | |||||||||||

| Provision for bad debt | 400 | |||||||||||

| 200,900 | 200,900 | |||||||||||