It is interesting that as an accountant, I have been learning a number of new things in accounting basics lately.

From the key elements of financial accounting to the accounting equations etc, I will admit it has been a process of unlearning and relearning. This is because, for the past few weeks, I am beginning to understand better some accounting concepts and conventions.

Let me give some credit to the Faculty. He has been painstakingly taking his time to explain and ensure that everyone is been carried along in the course.

One of my learning outcomes is the structure of accounting financial statements and other accounting documents. I learned that we have to use specific terminology to show that we understand the concept.

The faculty constantly emphasize the fact that we must understand the structure and arrangement of accounting transactions. In other words, once you understand the structure, the rest is history.

In his words, ”Corporate financial accounting relies heavily on structures”

TRANSACTION ANALYSIS

Let me quickly explain the flow of accounting transactions (Transaction analysis) as we go into the structures.

A transaction is any event that impacts the organization’s finances and can be reliably measured. In other words, it must be measurable financially.

Examples of transactions

A. Tommy limited purchased office supplies costing N35,000 on the 1st of April 202X.

B. On the 4th of April, Tommy limited paid cash of N800,000 to acquire a lot next to the campus for a business office building site.

The above two examples A and B are transactions. This is because they had an impact on Tommy Limited’s finances and we can reliably measure them.

JOURNAL VOUCHER

After we have identified the transaction, the next step is to enter it in a Journal Voucher also known as JV.

A Journal Voucher is a document in accounting that contains information about a financial transaction. The JV has the following information:

- Transaction date

- The Transaction amount

- Transaction description

- Accounts impacted

It is important to note that a JV has two sides for recording the transaction amount. The left and the right side. This is based on the double-entry system of accounting.

The left side is called the Debit side (Dr) and the left side is called the Credit side (Cr).

Every transaction affects at least two accounts, a receiving account, and a giving account. (I would like to refer you to my earlier post on Transaction analysis. This is where I explained the principles guiding when to debit or credit an account for further understanding).

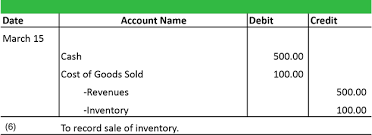

So, if we are to enter the example in “A” above into a Journal Voucher. We will expect it in the structure below:

You will notice, that the transaction date, the two accounts impacted, the amount and the description are all captured in the above.

Furthermore, we wrote the debited account first. The next was the credited account with a slight indentation to the right side.

My advice is; to create the Journal Voucher structure as seen above on your own so as to become part of you.

Hope you have learnt something useful.

Kindly watch out for my next post for the continuation.

Thank you.