If you’re looking to gain a comprehensive understanding of financial accounting, you won’t want to miss the third part of the series titled “So Far in Corporate Financial Accounting (CFA) – Part 2”. In the previous article, I provided valuable insights into the accounting cycle, accounting concepts, elements of accounting, and financial statements like income statements and balance sheets. In this latest instalment, I will delve into other key components of the balance sheet and explore transaction analysis in greater detail. By reading this article, you’ll gain a deeper understanding of financial accounting, which can benefit you both personally and professionally.

Balance Sheet

Liabilities

To put it simply just like Dr Francis explained it, liabilities are anything that the business owes another entity. In other words, it is the amount of money that needs to be paid by the business to settle its debts or fulfil any other financial obligations. This can include loans, accounts payable, taxes owed, or any other outstanding bills that the business is liable for. Understanding and managing liabilities is a crucial aspect of financial management for any business, as it helps to ensure the financial stability and sustainability of the organisation.

Current Liabilities

Current liabilities are obligations that are expected to be settled within a short period, typically within one year. Examples of current liabilities include accounts payable, short-term loans, accrued expenses such as salary owed to workers, and taxes payable.

Non-Current Liabilities

Non-current liabilities are obligations that are not expected to be settled within the next year. These are long-term liabilities that extend beyond the current operating cycle of the business. Examples of non-current liabilities include long-term loans, bonds payable, lease obligations, and pension liabilities.

Equity

Equity represents the ownership interest in a company. It represents the residual interest in the business’s assets after deducting liabilities. It represents the owner’s stake in the business. Equity can be divided into two main components: contributed capital and retained earnings.

Capital Structure

The capital structure of a company refers to the mix of debt and equity used to finance its operations. It represents the long-term financing sources of a company and includes long-term debt, equity, and other long-term obligations.

Financial Structure

The financial structure of a company is composed of its capital structure and short-term liabilities. It represents the overall composition of a company’s liabilities and provides insight into its financial health and risk profile.

💡 Finance short-term assets with short-term sources of funds and long-term sources of funds to long-term asset

Transaction Analysis

Transaction analysis is a fundamental concept in financial accounting that involves recording and analysing business transactions. It follows the double-entry accounting system, which states that every transaction has equal and opposite effects on at least two accounts.

The process of transaction analysis begins with the identification of the accounts affected by the transaction. Each transaction involves at least two accounts – one account is debited, and another account is credited. Debits and credits are used to record increases or decreases in different accounts.

The journal is the first step in the transaction analysis process. It is a chronological record of all transactions, where each entry includes the date, a description of the transaction, and the debited and credited accounts. The journal provides a detailed audit trail and serves as the basis for posting entries to the ledger.

The ledger is a collection of accounts where each account is dedicated to a specific asset, liability, equity, revenue, or expense. It contains the summarised and classified information from the journal entries. The ledger provides a central location for all account balances and allows for easy tracking and analysis of financial information.

The double-entry concept ensures that the accounting equation (Assets = Liabilities + Equity) remains in balance. For every debit entry made to an account, there must be an equal and opposite credit entry made to another account. This ensures that the total debits equal the total credits in the accounting system.

The Golden Rule

Dr Francis called it the golden rule of transaction analysis, and it is a mnemonic that is useful for transaction analysis. It is called DEAL-CLIP.

💡 DEAL CLIP DEAL – Debit all Expenses, Asset, and Losses CLIP – Credit Liabilities, Income, and Provisions

Dr FRANCIS OKOYE

Another way of understanding these is that anything that increases the asset account will be DEBITED from the account, and anything that decreases it will be CREDITED to the account. Anything that increases liability or equity will be CREDITED to the account, and anything that reduces liability will be DEBITED from the account

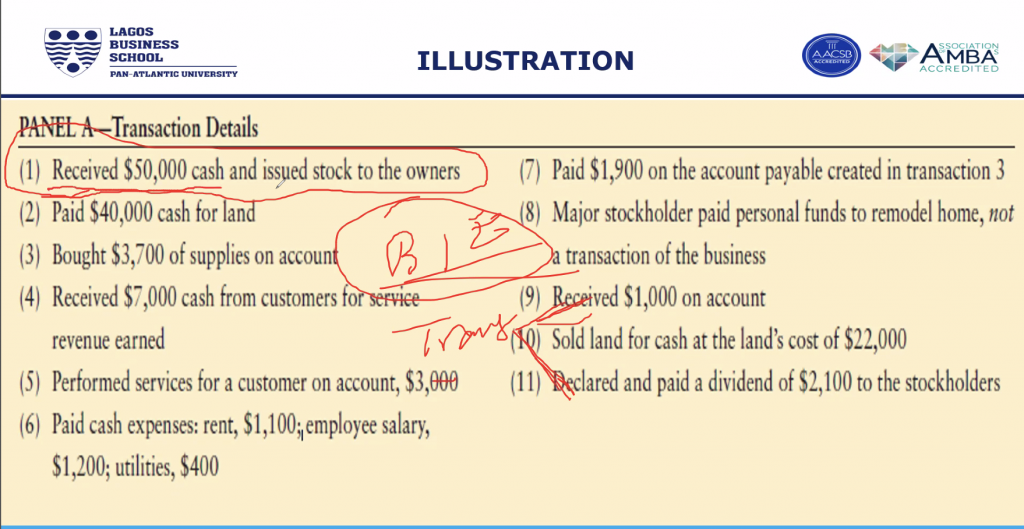

Using this rule, we were able to convert the transaction details below:

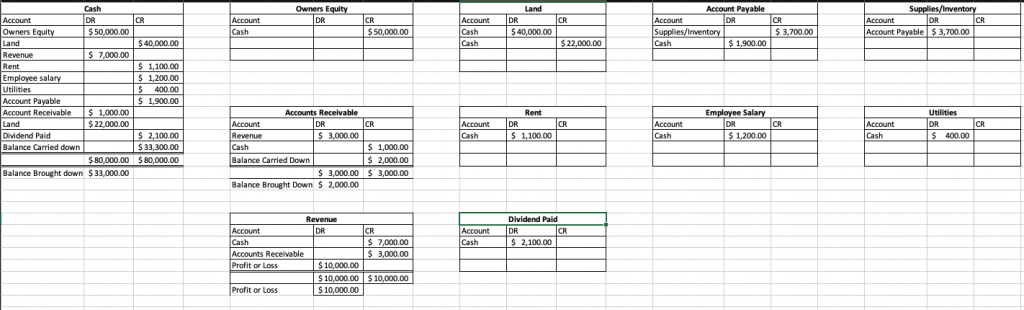

To these ledger entries:

From observing the different accounts, you will notice that most of the accounts are not yet balanced.

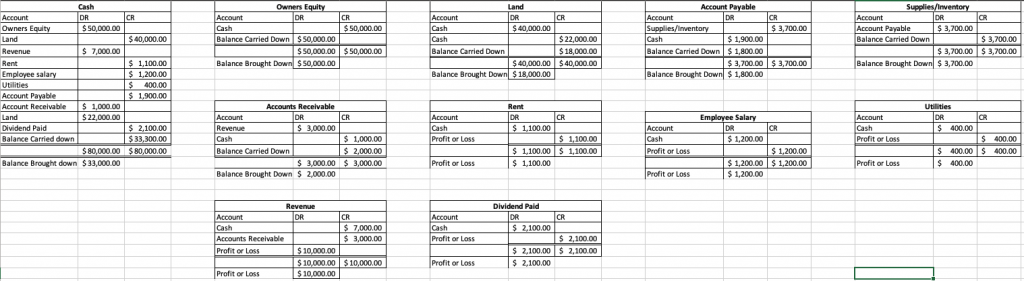

This is what the balanced accounts look like:

Conclusion

In the beginning of this series, we explored the difference between being busy and doing business. We learned about the importance of accounting in running a business and gained an understanding of the accounting cycles and the necessary elements required to implement solid accounting systems in a business. In this last article of the series, we covered the final part of the balance sheet (statement of financial position) and delved into transaction analysis using the double-entry concept.

By applying the double-entry concept in journal and ledger entries, businesses can accurately record and track their financial transactions. This enables them to generate accurate financial statements and make informed business decisions based on reliable financial information.

I hope you found this series informative and helpful. I would like to express my sincere appreciation to our facilitator and instructor, Dr. Francis Okoye, for providing clear explanations of accounting concepts, making it easier for people with no prior knowledge of accounting to understand.