This week, let’s turn our focus to the recently published capital importation data for Q3 and Q4 2022. For context, the capital importation data aggregates financial inflows (including credit and deposits) through the surveillance of banking transactions based on WTO classification systems. Additionally, physical capital imported is tracked leveraging customs data. From an economic relevance perspective, imported capital complements domestic savings and remittances to form investments for short-to-long-term economic expansion.

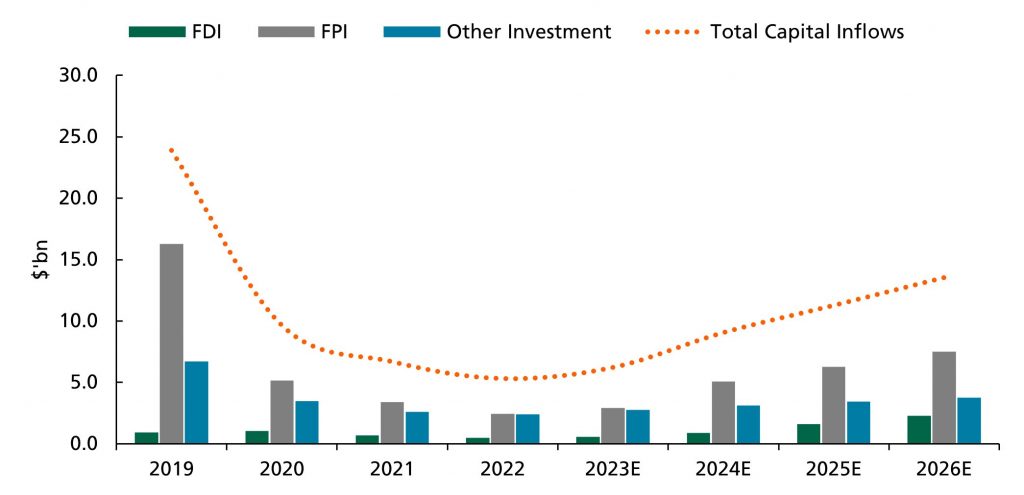

According to the Nigerian Bureau of Statistics, capital importation declined for the third straight year to $5.3bn (-20.5% y/y) broken down into inflows of $1.6bn, $1.5bn, $1.2bn, and $1.1bn for Q1, Q2, Q3, and Q4:2022 respectively. Notably, the FY print was 0.6 ppts lower than our forecast and the weakest inflow since $5.1bn in 2016. Disaggregating the data, Foreign Portfolio Investment (FPI) fell 27.9% to its six-year low of $2.4bn due to aversion to the money market (-46.3%) and equity (-72.6%) although investment in bonds grew 73.8%. Consequently, the share of FPI in total capital inflows dipped to 45.8% – the weakest since 2016 – against 50.5% in 2021. On the other hand, capital inflows from Other Investments fell 7.6% y/y to $2.4bn owing to a 2.8% decline in loans (96.3% of the sub-component). Despite the decline, the share of Other Investments rose to 45.4% which is the highest in at least 9 years. Also, Foreign Direct Investment (FDI) fell 33.0% to $468.1m while its size in the total capital inflows dropped to 8.8% from 10.4%. This suggests a continued decline in foreign investors’ interest in committing to long-term investment with the potential for wealth creation and sustainable growth in Nigeria.

Across sectors, Banking (39.2%), Production (17.8%), and Financing (14.8%) accounted for the most inflows as 8 sectors recorded growth and 12 declined. We note that non-financial activities accounted for only 37.1% of total inflows with funding heavily skewed to financial services. Similarly, Lagos (67.8%) and Abuja (30.6%) reported the lion’s share of capital inflows as only 10 states recorded inflows versus 13 in 2021. The heavy concentration in the economic and administrative capitals only highlights the poor state of sub-national economies in the country and the need to increase the attractiveness of states.

The poor business climate stemming from weak infrastructure, unsupportive policies, insecurity, and increasing poverty are some of the challenges that undermine the performance of capital inflows, especially FDIs. Therefore, measures that can help reverse ugly trends include the introduction of policies to support diaspora remittances, enhance crude oil production and diversify FX earnings. These policies would allow the CBN to reduce its reliance on capital controls to manage FX reserves and, in turn, the free flow of capital would reduce the apathy of foreign investors to the domestic market. Additionally, the issue of multiple FX windows should be addressed while the business environment should be enhanced by investing in infrastructure and undertaking necessary reforms across key sectors of the economy.

For FY:2023, it is expected that capital flow will hit $6.2bn. This reflects the slowdown in investment activities in Q1:2023 due to the election uncertainty and the cost of delayed fiscal normalization until H2:2023 and extended policy tightening in Advanced Economies.

#MMBA4

Financial Ratios and Interpretation

Financial Ratios and Interpretation