Understanding how to pass journal entries logically with the use of debit and credit is a fundamental learning point for those who want to have a grasp of accounting.

Most people get confused with the usage of debit and credit in accounting. They interpret credit to mean positive and debit to mean negative. These are misconceptions that we will clarify in this write-up.

The first step of accounting is recording the financial transaction, next is to classify them into standard formats, and lastly to summarize them into financial statements like the statement of profit and loss, cash flow statements, and so on.

The journal entry comes under the first step of recording financial transactions. To record any financial transaction, an accountant passes entries with debit and credit in a book called a journal. The entries to be passed in the journal are found in the source document; evidence of the transaction that proves that the transaction has occurred.

Below is a snapshot of the accounting process:

| Source document | → | Journal | → | Ledger | → | Trial balance | → | Financial statements |

Our focus, however, is the journal entry.

The rules of debit and credit, we look at the modern approach.

| D | E | A | L | E | R |

| Drawings or Div | Expense | Asset | Liability | Equity | Revenue |

Drawing: when an owner invests in his business, it is called capital, and when the owner withdraws the money for personal use, it is called drawings. This happens in a partnership or single-partner business.

Dividend: in companies, capital is divided into small units called shares, the owners are called shareholders who are owners of the company. These people get dividends in form of returns. Here, we don’t have single capital, we have Equity share capital (Equity)

Asset: An asset is a resource controlled by an entity as a result of past events and from which future economic benefits are expected to flow to the entity. E.g. Computers, furniture, and buildings.

Expense: cost of operation that a company incurs in other to generate revenue and from which no further benefit is expected. E.g. Rent, salaries, and utility bills.

Liability: a financial obligation as a result of a past event. E.g. Loans.

Revenue: income from sales.

Now, to understand the rules of debit and credit.

The rules of debit and credit, we look at the modern approach.

| D | E | A | L | E | R |

| Drawings or Div | Expense | Asset | Liability | Equity | Revenue |

| DEBIT BALANCE | DEBIT BALANCE | DEBIT BALANCE | CREDIT BALANCE | CREDIT BALANCE | CREDIT BALANCE |

| DR. ↑ CR. ↓ | DR. ↑ CR. ↓ | DR. ↑ CR. ↓ | CR. ↑ DR. ↓ | CR. ↑ DR. ↓ | CR. ↑ DR. ↓ |

To increase the D.E.A, you debit them, and to decrease them, you credit them as visualized above. Vice versa for L.E.R. Further broken down below:

| BALANCE | INCREASE | DECREASE | |

| DRAWINGS | DEBIT | Dr. | Cr. |

| EXPENSE | DEBIT | Dr. | Cr. |

| ASSET | DEBIT | Dr. | Cr. |

| LIABILITY | CREDIT | Cr. | Dr. |

| EQUITY | CREDIT | Cr. | Dr. |

| REVENUE | CREDIT | Cr. | Dr. |

For example; furniture, this is controlled by the entity and has future economic benefits, therefore, it is an asset. So, to increase it, we debit, and to decrease it, we credit.

You should be able to classify anything into the 6 accounts (D.E.A.L.E.R), e.g. computers, land, buildings, credit card, electricity, etc.

P: N. There is no meaning to debit and credit, they are two abstract terms we use in accounting to reflect the duality concept (double entry), we record every transaction with a debit and a credit, and both effects are always equal. This an accounting convention that cannot be explained; it just is, and we just take it.

Before passing a journal entry, it is important to learn the technique of journalizing:

- Analyze the transaction.

- Identify at least two accounts involved in the transactions. Double entry system.

- Find in which category they fall (DEALER).

- See if they are increasing or decreasing.

- Use the DEALER rules.

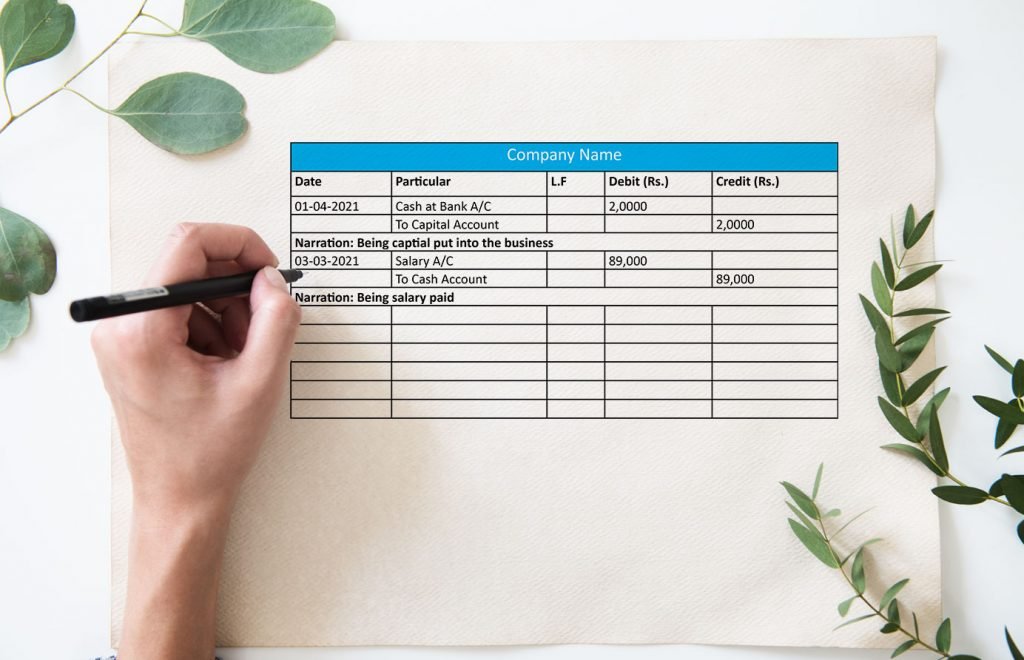

Example: Bayo started a business with cash of N1,000,000.

Solution:

Look at it from the point of view of the business.

The accounts affected here are cash and equity.

Cash is an asset, therefore:

| Dr. | Cr. | ||

| 19/10/2022 | Cash account | 1,000,000 | |

| To Capital account | 1,000,000 | ||

| Narration: being capital put into the business |

#MEMBA11

Analysis of Business Problems – Problem Statement

Analysis of Business Problems – Problem Statement