“The balance sheet is a company’s DNA. It tells you what the company is made of.”

-Marty Whitman.

The significance of corporate financial accounting has assumed a greater level of importance across the world in recent times due to its perceived importance as a driver of organizational growth, especially in for-profit organizations. The significance and understanding of the components of the financial statements cannot be over-emphasized given the level at which companies’ poor decisions are leading to financial instability, loss of market share, and ultimately business failures.

There are four basic financial statements which are often referred to as the Four plus one, they include:

a. The Balance Sheet

b. The Cash flow

c. The Statement of Income

d. The statement of owner’s equity

and the notes to the financial statements.

However, the focus of this article will revolve around the concept, components and application of the balance sheet which tells the financial position of a company at a particular period shall be explained.

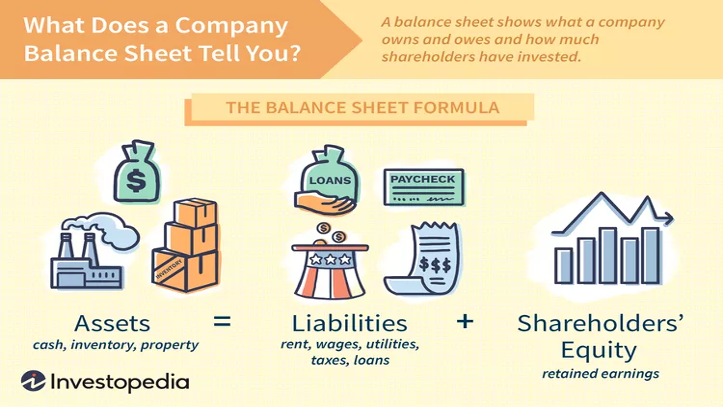

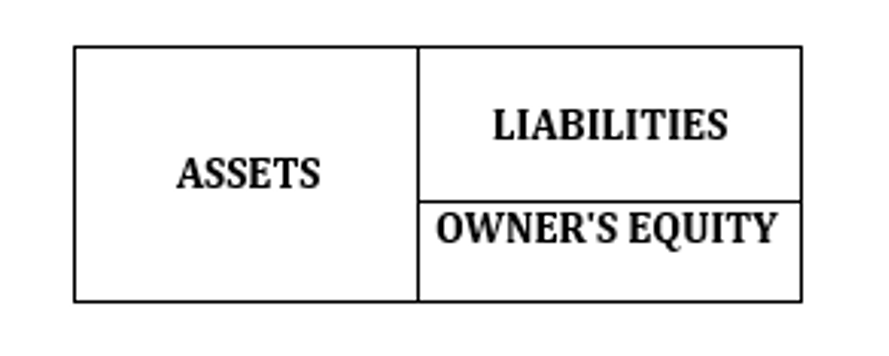

The Balance Sheet is a financial report that provides a general overview of a company’s financial health at a specific time. It is considered a cursory picture of a company’s financial status – an essential tool for investors, lenders, and decision-makers to assess its financial standing and make informed decisions.

It gives an insight into the kind of resources available to the company and details of the sources it used in generating the resources; what analysts refer to as assets. The total of the company’s liabilities and the owner’s equity is how you ascertain the nature and extent of the said assets. Assets can therefore be defined as both tangible and intangible resources that the company owns and controls which can usually be measured in monetary terms and has the potential of providing future economic benefits to its owners. Assets are categorized into two main components:

- Current Assets

- Non-Current Assets

Current assets: These are assets that are expected to be used up within the operating cycle. Examples are Cash and cash equivalent, Accounts receivable, Inventory and prepaid expenses.

Noncurrent assets: These are assets that are expected to be in use over a longer period and are not expected to be used up over the financial cycle. Examples are property, plant and equipment, Intangible assets, investments and long-term loan receivables.

Liabilities are commitments made by the company to repay monies owed to external parties which represents a claim against the company’s asset. Liabilities are categorized into 2 main components:

- Current Liabilities

- Non-Current Liabilities

Current Liabilities These are liabilities that are expected to be paid over a business cycle. Examples are Accounts payable, short-term loans, and income taxes payable.

Non-Current Liabilities: These are liabilities that are not expected to be settled within the given financial cycle.

Owner’s Equity: it can also be referred to as shareholders’ equity. This represents the amount contributed by the owners of the company. The components of owner’s equity include Stocks, Additional paid-in capital, Retained earnings, Reserves, and non-controlling interest.

Hence, the balance sheet can be represented thus: A= (L+ OE). This therefore implies that the total Assets of a company must be equal to its liabilities plus the owner’s equity.

Summarily, the balance sheet readily avails the company’s management, shareholders and investors the opportunity to, at a glance, assess risks and opportunities inherent within the financial position of the company.

#MEMBA12

Unlocking Efficiency: Strategies for Getting More Done in Less Time.

Unlocking Efficiency: Strategies for Getting More Done in Less Time.