A key principle of accounting used to guarantee the accuracy and completeness of account records is double entry. It is based on the assumption that each financial transaction involves at least two or more accounts, with at least one account debited and at least one account credited. This concept shall be applied to the recording and summarising of transactions, establishing a basis for preparation of accounts and other reports.

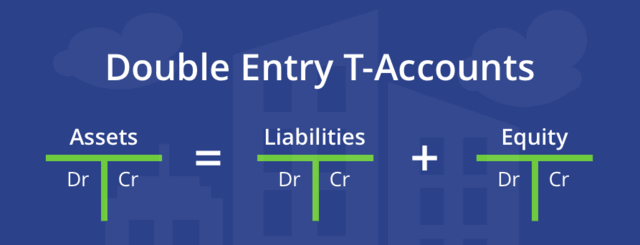

The concept of a double entry is based upon the equation: Assets = Liabilities + Equity. The accounting equation is called the accounting equation and it must be maintained at a constant level in order to have accurate financial statements. The double entry system makes sure that the corresponding credit entries in another account are available for every debit transaction carried out on a single account.

The concept of double entries works by recording each transaction in two or more accounts, with debits and credits balancing each other. For example, if a company bought stock in cash, it would debit an inventory account and credit its cash account. This ensures that the total value of the company’s assets will remain constant, although its composition has changed.

The provision of a system of checks and balances is one of the most important advantages of this dual entry concept. Because each transaction is made up of a minimum of two accounts, error and fraud can become harder to detect. As all transactions shall be entered in a uniform and harmonised way, the dual entry scheme also facilitates the preparation of accurate financial statements and supplementary reports.

Furthermore, the double entry concept will provide more precise information on a company’s financial situation. By recording each transaction in multiple accounts, they will be capable of monitoring financial flows and identifying business areas where the firm generates or loses money. It is also possible for the company to make informed decisions about its next course of action and identify areas in need of adjustment or improvement.

The distinction between debit and credit entries should be clearly understood in order to effectively use the double entry system. Debits shall be recorded on the account’s left margin, representing an increase in assets or a decrease in liabilities or equity. By contrast, credits are recorded on the left side of an account and they represent increased indebtedness or equity or a decrease in assets.

Conclusion: The principle of double entries used to ensure that the financial statements are precise and complete is a fundamental accounting principle. This is based upon the concept of at least two accounts being part of every transaction, with one account to be used for debiting and another as a credit. The double entry system provides a system of checks and balances, makes it easier to prepare accurate financial statements, and provides more detailed information about the financial health of a company. For anyone in the area of accounting or finance, it is essential that they understand double entry so as to be able to record and summarise transactions.

MMBA4

THE CAMELS APPROACH-TOOL BY FINANCIAL SERVICES INSTITUTION- PART2

THE CAMELS APPROACH-TOOL BY FINANCIAL SERVICES INSTITUTION- PART2