We had at a prior session on #EMBA 28 ABP analysed the case of Alusaf, the sole primary aluminium producer in South Africa is considering building the world’s largest greenfield primary aluminium smelter – the Hillside Project producing 466,000 metric ton-per-year. The company has carried out a feasibility study on the project during the past 2 years. However, new developments and uncertain industry conditions is pushing the managing director Rob Barbour to reconsider embarking on the Hillside project.

Rob Barbour is skeptical about embarking on the project considering its enormous size and capital intensity. Rob and the Alusaf Team is faced with the decision of committing to the Alusaf Hillside Project or withdrawing from the project.

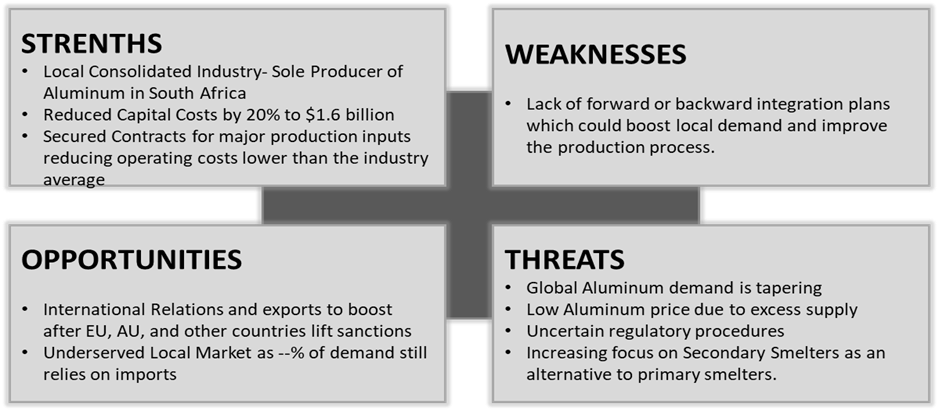

Industry Analysis

Although the Project has ample opportunities to explore, the lurking threats and risks cannot be overlooked as it determines the extent to which the opportunities can be explored to recoup benefits. See Chart 1. The Hillside project is not a viable project for Alusaf to embark on at the moment. Key Pointers in the global and Domestic industry are analysed below:

Pricing: Unstable Price of Aluminium

Considering the importance of aluminium price and its integration into the cost structure of the hill-side project, price plays the most important role in determining how viable the project is. On the back of the global excess supply of 1.3mn tpy and plummeting global consumption, global aluminium price fell to its lowest at $1,100 per ton. Despite the voluntary production cut agreed by major aluminium producing countries, price increased very slow in early 1994 to reach $1,110. It is largely unclear whether prices would recover fully soon. So, in a bid to stabilize prices, it is expected that production volume will continue to be tapered posing a threat to profitability of the Hill-side project.

The Secondary Smelter- A growing alternative to primary smelters

Secondary smelting production is becoming increasingly popular accounting for about a quarter of world production in 1994 with a 10-year CAGR production of at 3.7% compared to the 1.4% of primary smelters. While the primary smelters like Hillside project are still majorly used in the industry, the secondary smelters are more efficient in size, capital intensity, and cost maximization as it consumes only about 5% of the energy ton of a primary smelter. Secondary smelters represents 15% of the total domestic production in South Africa at 30,000tpy. It is evident that the industry production structure might change in coming years towards more affordable processes as seen in Japan, Russia, and Canada. This poses a threat to the hillside project sustainability and a possibility of a high barrier to exit.

Chart 1: Internal and External Analysis

Cost Analysis

Capital Cost Estimates: Equipment suppliers quoted Alusaf prices 20% to 30% below the $2 billion projected for the feasibility study, and the capital cost of the new plant is estimated to total $1.6 billion, a 20% discount from previous projected- See Table 1. The reduction is an incentive for Alusaf to embark on the hill side project. However, the project’s proposed installed capacity might not be optimally utilized due to the regulation of global production volume. Moreover, the computed return on asset and asset turnover of large aluminium firms indicates an underperforming total asset base in the industry. While return of Assets has been substantially negative, asset turnover is within the 0.68 and 0.89 range. See Table 2

Table 1: Capital Cost Structure

| Feasibility Study Projection | New Projection | % Change | |

| Capital Cost | $2 billion | $1.6 billion | -20% |

Table 2: Industry Performance Summary

| Alcoa | Alan | Reynolds | Pachiney | Alumax | Kaiser | Norsk | |

| Asset Turnover | 0.78 | 0.74 | 0.79 | 0.89 | 0.79 | 0.68 | 0.69 |

| Return on Asset | 0.04% | -1.06% | -4.80% | -1.24% | -4.66% | -25.79% | 3.40% |

Operating Costs Estimates

Having computed the operating costs and estimated income of the project in relation to the industry’s average. The total operating costs of the hillside project is 32% lower than the industry’s average as seen in Table 3 indicating a favourable cost structure accruing to the long-term contracts on electricity and Alumina inputs for production process. Moreover, Table 4 shows that at current price of $1,110, the hill side project has the potential to make $285 per metric ton as compared to the $-100 of the industry average. Nonetheless, it is important to note that this figure is attainable if prices trend higher or become stable. However, with high uncertainties surrounding prices and global consumption volumes, A further fall in price will be putting the project in a difficult ditch.

Table 3: Operating Cost Structure per Aluminium Ton. Industry Average Vs Hill-Side Project

| Average Smelter | Hill-Side Project | |

| Electricity and Alumina | 685 | 455 |

| Other Raw materials | 125 | 143 |

| Plant, Power and Fuel | 10 | 17 |

| Consumables | 70 | 32 |

| Maintenance | 50 | 38 |

| Labour | 150 | 68 |

| Freight | 45 | 40 |

| General and Administrative | 75 | 32 |

| Total Operating Costs | 1,210 | 825 |

Table 4: Estimated income Per Ton. Hill-Side Project Vs Industry Average

| Average Smelter | Hill-Side Project | |

| Aluminium Price per ton | 1,110 | 1,110 |

| Total Operating Costs | 1,210 | 285 |

| Estimated Income per Ton | (100) | 285 |

Decision Recommendation

Alusaf should not embark on the Hillside project. Suggested Strategic alternatives for Rob Barbour and the Alusaf team are:

- to delay the launch of the Hillside project until market conditions show indications of stabilizing into the long-term or

- pursue a small-scale expansion project to increase its existing capacity so as to better serve the local market.

- Integrate forward into fabrication of the Aluminium ingot.