One of the interesting topics we treated in our last sessions of CFA (Corporate Financial Accounting), was the Statement of cash flow. I believe many of us use to come across it in some companies’ financial reports. Although, some people may not necessarily pay attention to it. Especially, those who dislike or grow away from numbers. By now after attending the last lectures, one must have had an insight or idea of what a statement of cash flow is all about.

It is statutory or required by law and or accounting standard that every company should disclose its financial statement. Out of which include a statement of cash flow. In other words, It is one of the three financial statements that companies are required to prepare for external reporting purposes, along with the balance sheet and income statement.

The statement aims at providing details information about the net cash flow, that is inflows and outflows of the business for a given period, usually one year. That is why, the heading use to be clearly stated as:

“Statement of Cash Flows for the Year Ended 31 December, 20XX.”

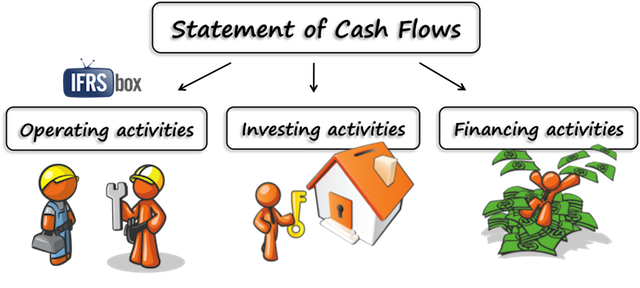

It is important to know that there are three (3) major components of a cash flow statement, Operating, Investing, and Financing activities. They are as follows:

- Operating activities: This section shows the cash inflows and outflows from a company’s main business operations. These cash flows can include payments to suppliers, collections from customers, and payments to employees.

- Investing activities: This section shows the cash inflows and outflows from a company’s investments. These cash flows can include the purchase or sale of property, plant, and equipment, as well as investments in other companies.

- Financing activities: This section shows the cash inflows and outflows from a company’s financing activities. These cash flows can include borrowing or repaying loans, issuing, or buying back stock, and paying dividends to shareholders.

Apart from the components, another important aspect to look at is the method of computing cash flow statements. Many accounting texts books and ICAN FAQs emphasize only methods, Direct and Indirect methods.

However, we only discussed on Indirect method in our last class. Where the facilitator detailly explained to the layman understanding.

Indirect Method

This method started with the Profit before tax which is the accounting profit computed in the statement of profit or loss. It is believed that before arriving at the profit amount, many non-cash items were included. Such items are mere estimated amounts base on a certain accounting principles and assumptions that need to be adjusted for the purpose of cash flow calculations.

The facilitator used a suitable format that complies with the IAS (International Accounting Statement) 7, and thus:

Statement of Cash Flows for the Year Ended 31 December, 20XX

N’000 N’000

Profit before tax XX

Adjusted for:

Depreciation x

Income from Investment x

Income expense (x) x

Movement in Working Capital:

Decrease/Increase in Inventories x/(x)

Decrease/Increase in Receivables (x}/x

Decrease/Increase in Payables x/(x)

Interest paid. (x)

Tax paid (x) (x)

Net cash flows generated from operating Activities X

The above format is what differentiates the two methods.

In conclusion, a cash flow statement is important because it shows how a company is managing its cash. A company can generate a lot of revenue, but if it is not managing its cash flow well, it may not be able to pay its bills or invest in growth opportunities.

Investors and other stakeholders can use the cash flow statement to assess a company’s financial health and performance. For example, they can look at the operating cash flow to see if the company is generating enough cash from its operations to cover its expenses. They can also look at the investing and financing cash flows to see how the company is investing in its future and how it is financing its growth.

What is E-Waste?

What is E-Waste?