In continuation of the write up on my learning experience from Lagos Business School EMBA 28 on the Corporate Financial Accounting class, anchored by Professor Owolabi.

We began with MODULE 1, having two sessions covering the following topics:

- Users and suppliers of financial statement information.

I started by exploring the ( a) part in my last post, I will continue this week from the topic number (b)

- The four financial statements, and the accounting equation.

FINANCIAL STATEMENTS

Companies use four financial statements to periodically report on business activities. These statements are the: balance sheet, income statement, statement of changes in equity, and statement of cashflows. A balance sheet reports on a company’s financial position at a point in time. The income statement, statement of changes in equity, and the statement of cash flows report on performance over a period of time.

Balance Sheet

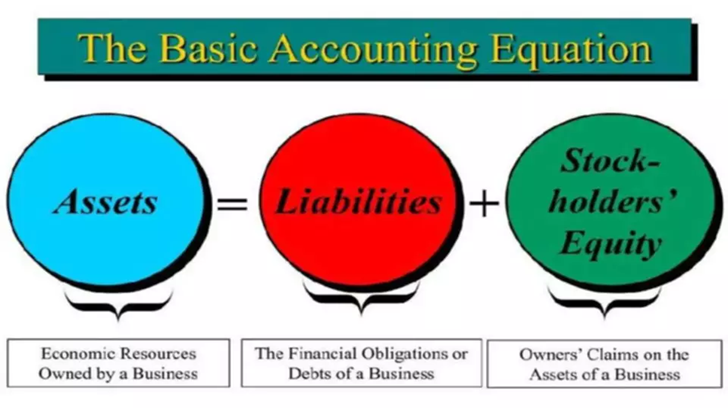

A balance sheet reports a company’s financial position at a point in time. The balance sheet reports the company’s resources (assets), namely, what the company owns. The balance sheet also reports the sources of asset financing. There are two ways a company can finance its assets. It can raise money from shareholders; this is owner financing. It can also raise money from banks or other creditors and suppliers; this is nonowner financing. This means that both owners and nonowners hold claims on company assets. Owner claims on assets are referred to as equity and nonowner claims are referred to as liabilities (or debt). Since all financing must be invested in something, we obtain the following basicrelation: investing equals financing. This equality is called the accounting equation, which follows:

| INVESTING = | NON OWNER FINANCING + | OWNER FINANCING |

| ASSETS = | LIABILITIES + | EQUITY |

If you don’t know how to read and analyze a Balance Sheet, read this:

A balance sheet is a snapshot of a business at a specific point in time.

It serves two purposes.

Internally, it provides information about the financial health of a company.

Externally, it depicts the business’s resources and how they are financed.

It shows the company’s assets, liabilities, and shareholders’ equity.

The accounting equation works for all companies at all points in time.

Investing Activities

Balance sheets are organized like the accounting equation. Investing activities are represented by the company’s assets. These assets are financed by a combination of non-owner financing (liabilities) and owner financing (equity).

Financing Activities

Assets must be paid for, and funding is provided by a combination of owner and non-owner financing.

Owner (or equity) financing includes resources contributed to the company by its owners along with any profit retained by the company.

Non-owner (creditor or debt) financing is borrowed money.

We distinguish between these two financing sources for a reason:

borrowed money entails a legal obligation to repay amounts owed, and failure to do so can result in severe consequences for the borrower.

Equity financing entails no such legal obligation for repayment.

The relative proportion of nonowner (liabilities) and owner (equity) financing is largely determined by a company’s business model.

Below are some examples of items that fall under each section:

- Assets: Accounts Receivable, Inventory, Property, Plant and Equipment

- Liabilities: Accounts Payable, Long-term Debt

- Shareholder’s Equity: Share Capital, Retained Earnings

Rearranging the Accounting Equation

The accounting equation can also be rearranged into the following form:

Shareholder’s Equity = Assets – Liabilities

In this form, it is easier to highlight the relationship between shareholder’s equity and debt (liabilities). As you can see, shareholder’s equity is the remainder after liabilities have been subtracted from assets. This is because creditors – parties that lend money such as banks – have the first claim to a company’s assets.

For example, if a company becomes bankrupt, its assets are sold and these funds are used to settle its debts first. Only after debts are settled are shareholders entitled to any of the company’s assets to attempt to recover their investment.

Regardless of how the accounting equation is represented, it is important to remember that the equation must always balance.

Watch out for the remaining topics under Module 1 in my next blogging. Thank you for reading.

Democracy, Governance and Citizens Welfare

Democracy, Governance and Citizens Welfare