Financial accounting is the process of recording, summarizing, and reporting financial transactions of an organization to provide useful information to stakeholders. These stakeholders include investors, creditors, regulators, management, and the public. Financial accounting plays an essential role in decision-making, such as investing in a company, extending credit, and analyzing financial performance.

The process of financial accounting starts with the recording of transactions in a systematic and organized manner, also called a journal. Each transaction is recorded with a debit and credit, which is an accounting method used to ensure the accuracy of the financial records. Examples of such transactions are sales, purchases, payments, receipts, and borrowing.

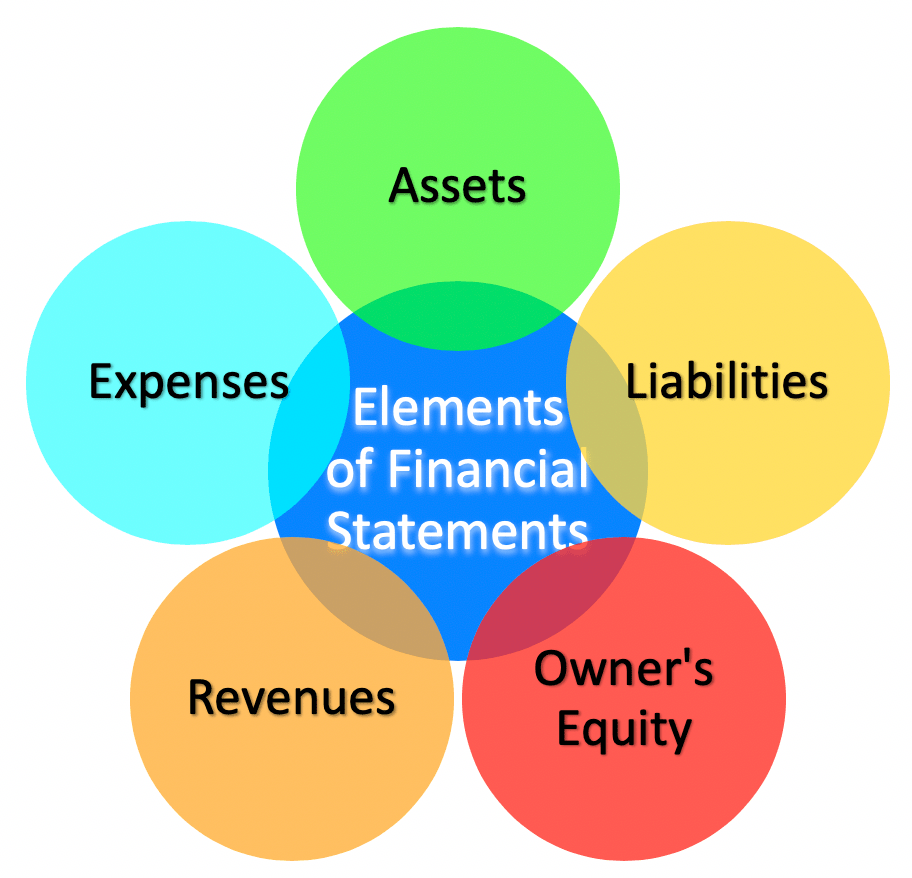

The three primary financial statements are the income statement, balance sheet, and statement of cash flows. The income statement reports the organization’s revenues and expenses for a specific period and shows whether the organization has made a profit or loss. The balance sheet reports the organization’s assets, liabilities, and equity as of a specific date and shows the organization’s financial position. The statement of cash flows reports the organization’s cash inflows and outflows for a specific period and shows the organization’s ability to generate cash.

The income statement reports an organization’s revenue, expenses, and net income or loss for a specific period. It shows the organization’s profitability and ability to generate income. The balance sheet reports an organization’s assets, liabilities, and equity as of a specific date. It shows the organization’s financial position and whether it is solvent or insolvent. The statement of cash flows reports an organization’s cash inflows and outflows for a specific period. It shows the organization’s ability to generate cash from its operating activities, investing activities, and financing activities.

Financial accounting also involves the use of accounting principles and standards to ensure consistency and comparability in financial reporting. The Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS) are the two most widely recognized accounting standards. These standards provide general guidance on how to record and report financial transactions, which ensures that financial statements are reliable, consistent, and comparable.

In addition to financial statements, financial accounting also involves the preparation of other reports. These reports may include management reports, tax returns, and regulatory filings.

In conclusion, financial accounting is a vital aspect of business that involves recording, summarizing, and reporting financial transactions. The primary objective of financial accounting is to provide stakeholders with useful information to aid decision-making. The use of accounting standards ensures consistency and comparability in financial reporting, while financial analysis provides insights into an organization’s financial performance and position.

Theoretically, this looks easy to understand, right?

Once we get to the practical aspect and how to apply the debit and credit accounting principle(s) as it relates to Assets, Liabilities, Owners Equity, etc., I am looking to the God of miracles because I can tell you that these Accounting Principles are turning on its own to a layman like me.

O God of miracles, it is well …

#EMBA28