If you are a beginner like me, learning how to prepare any financial statement or book of account such as a journal, ledger, balance sheet, profit statement and the likes, you are bound to encounter seemingly questionable comments from the Lords of the profession such as: “this is how it is done”, “that is the rule of the profession”, “this is the rule of trade”, and many other similar expressions that you have no choice but to accept and live with.

Although, questioning the rationale behind some of these ground rules may be a smart move, it is, no doubt, a recipe for disaster, as it could block your mind from accepting and applying new knowledge to achieve growth and become a better manager. Reflecting on the teachings of Prof Akintola during his Corporate Financial Accounting (CFA) Executive MBA class at the Lagos Business School, I wondered if being a great manager implied abiding by the existing rules laid down by the grandfathers of the profession or ripping them apart for fresh approaches that may evolve into a new and better knowledge accepted for another set of generations.

But who am I kidding? I still needed to at least comprehend and accept the idea that an increase in an asset should be recorded as a Debit in a “T-account”, a fancy name for a way to record daily changes in financial transactions a corporate organization embarks on. Anything else could be the end of my recent romance with accounting, a subject I last came in contact with back in my secondary schools days over 20 years ago.

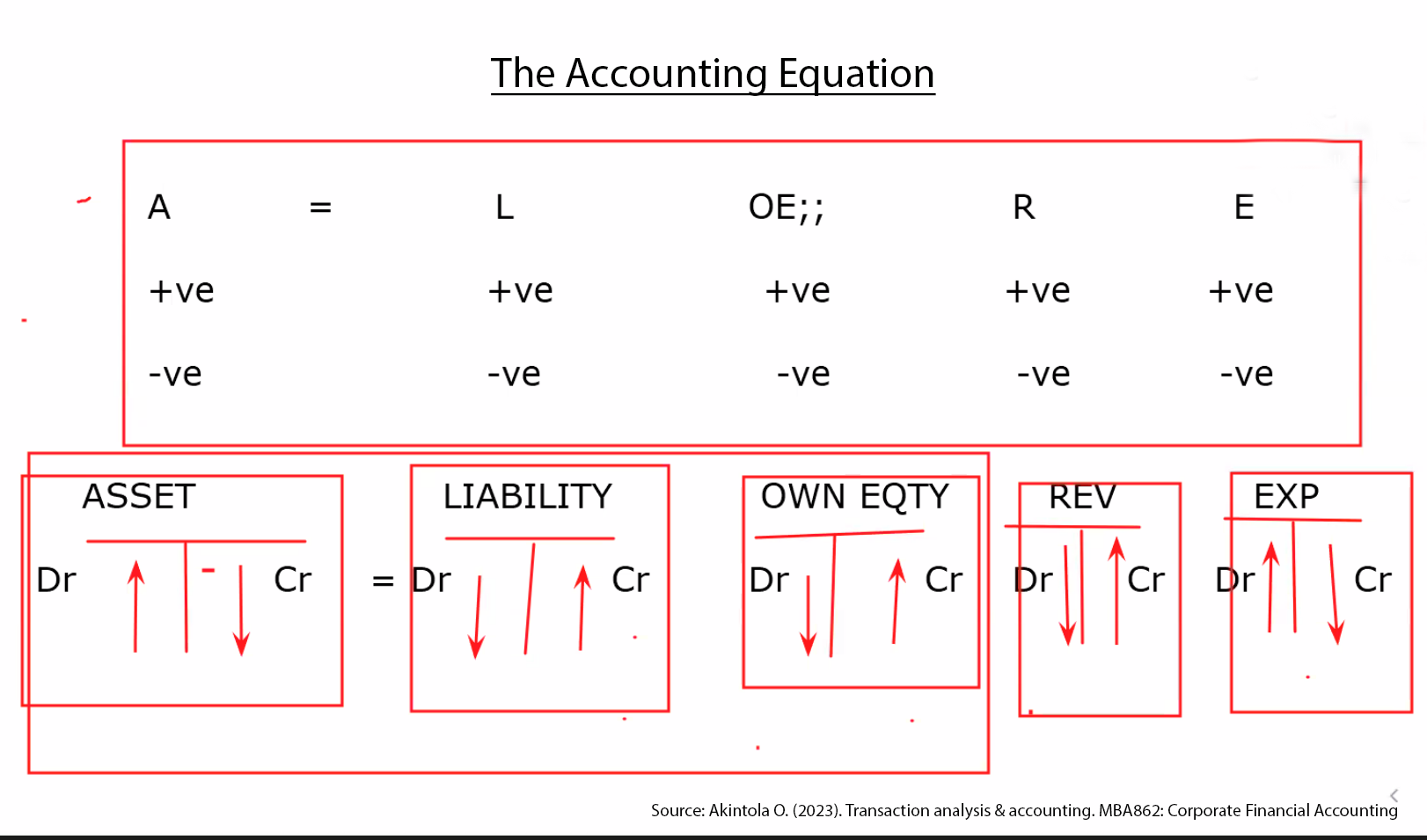

Prof called it a form of Double Entry, implying that transactions must be registered in two separate accounts which captures its dual effect on an entity (i.e., a corporate organization). Each of these accounts are called T-accounts represented by the letter T with the left side of the T titled Debit and the right side, as you would have guessed, titled Credit.

Listening to Prof, I could almost detect the excitement from my other colleagues as we all nodded our heads in agreement. And why not? We had all seen this formular at our places of work irrespective of industry and designations. Plus, it made sense that Debit should be placed on the left and Credit on the right side of the illustrious Mr. T., a name Otaoghene, our class comedian had quickly came up with.

But how our eyes opened in initial surprise when Prof announce that an increase in asset is registered as a debit. We all looked at each other in obvious confusion. Well, except of course, our colleagues with finance background who were visibly smiling at our ignorance. “Does that also suggest that a decrease in asset is registered as a Credit then?”, someone from behind had questioned hoping maybe it was just an error Prof would immediately correct. But his baritone response of “That is correct”, echoed through the now quiet classroom. “This means that a business that receives cash, for example, will debit the cash account, but will credit the account if it pays out cash”, he added.

As confusing as it may have sounded right there in class, Prof’s style of ensuring all students participated in his many class exercises was the antidote we needed to finally come to terms with this rule. But did it apply to the other components that make up the accounting equation? If an increase in Asset component is marked a debit, does this also suffice with Liability and Owners equity? I promise to share my experience in one of my subsequent blogs.