Every financial transaction has equal and opposite consequences in at least two independent accounts, according to the fundamental principle of double entry, which underpins modern bookkeeping and accounting. In a general ledger or T-account, transactions are recorded using the double-entry approach as debits and credits. The total of all debits must equal the total of all credits because a debit in one account cancels out credit in another. With this system, the accounting process is standardized, created financial statements are more accurate, and errors are easier to spot.

T-Account

A collection of financial records that employ double-entry accounting is referred to informally as a T-account. The phrase defines how the bookkeeping entries appear. On a page, a huge letter T is first drawn. The account name is then written directly above the top horizontal line, and below that, split by the vertical T of the letter, debits are reported on the left, and credits are recorded on the right.

Debits and credits may represent increases or decreases for various accounts, but they must always be reported with the debit side to the left of the T outline and the credit side to the right. Following the completion of any financial transaction, a T-account can be used to depict the three main elements of the balance sheet: assets, liabilities, and shareholders’ equity.

When an asset account is debited, the account is increased; when it is credited on the right side of the asset T-account, the account is decreased. In other words, if a company receives cash, it will debit the asset account; however, if it disburses cash, it will credit the account.

In a T-account, the liabilities and shareholders’ equity (SE) debit entries reduce the accounts, while any credits show an increase in the accounts. A corporation will have an increase in its asset account and a comparable increase in its equity account on its T-account if it issues shares, for instance.

Adjusting entries are frequently prepared using T-accounts. According to the accrual accounting matching principle, all expenses and income for the period must match. The T-account instructs accountants on how to enter information in a ledger to obtain an adjusting balance, ensuring that revenues and expenses are equal.

T-accounts can also be used by a business owner to extract data, such as the type of transaction that happened on a specific day or the balance and activity of each account.

Trial Balance

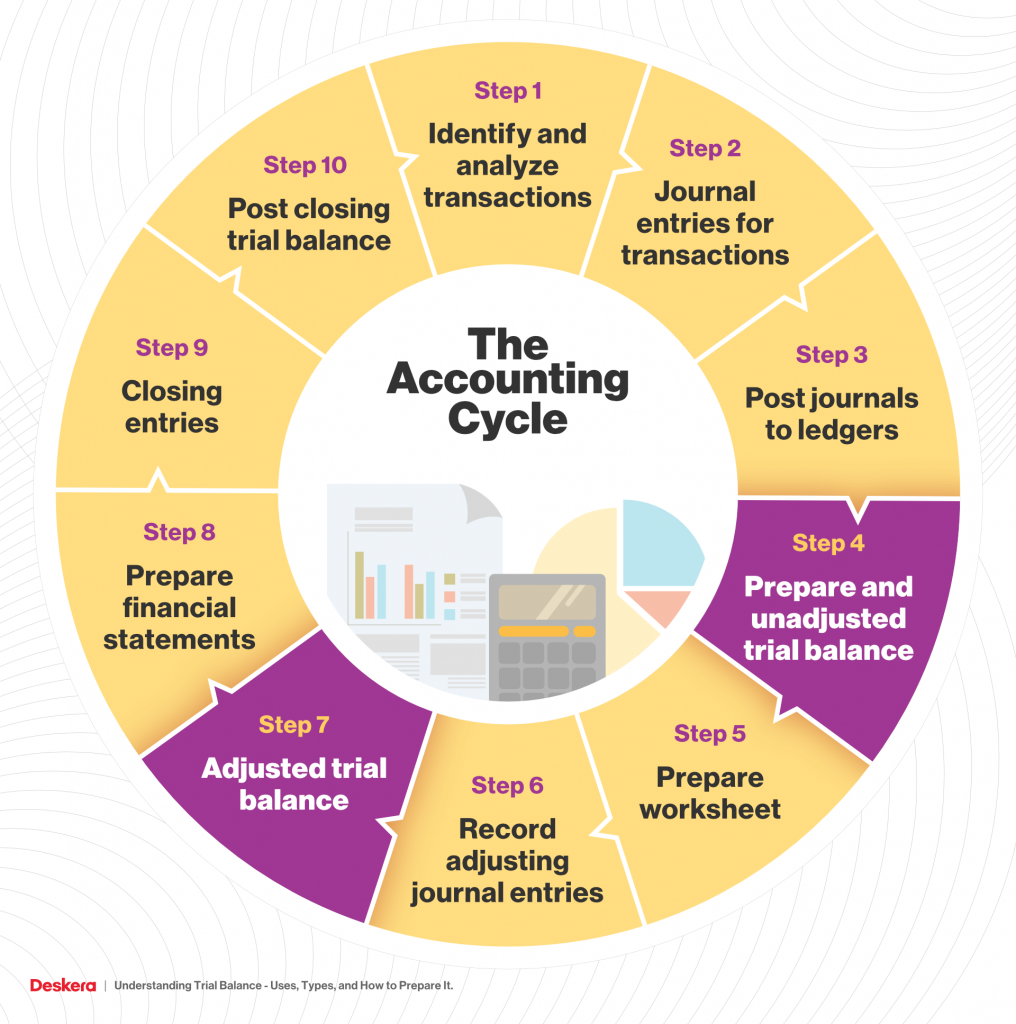

A trial balance is an accounting worksheet where the balances of all ledgers are totaled into equal amounts in the columns for the debit and credit accounts. A corporation occasionally creates a trial balance, often at the conclusion of each reporting period. To check that the entries in a company’s bookkeeping system are mathematically correct, a trial balance is generally produced.

A trial balance is not a complete audit of the accounts; rather, it tests a key component of the books in question. A trial balance is frequently the first step in an audit process because it enables auditors to confirm that the bookkeeping system does not contain any mathematical errors.

#MEMBA11