In my previous blog post, I wrote about journal entries and how to pass them. I showed how the D.E.A.L.E.R approach is used to identify what account to debit and which to credit.

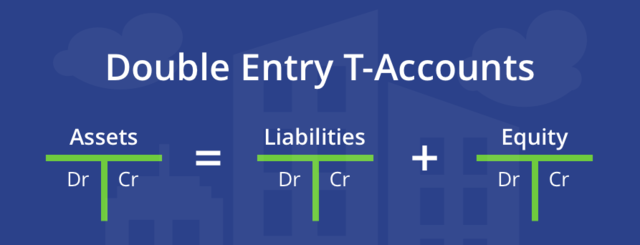

I will be looking at the golden rule of accounting, also known as the double-entry rule. This is the rule that guides entries that we make in the ledger. The rule was devised by an Italian monk called Fra Luca Pacioli in 1941. According to the rule, every business transaction must have two parties to the transaction, and every transaction affects each of the parties twice; this is why it is called a double entry.

The rule states that every debit entry must have a corresponding credit entry and vice versa.

This means that every transaction that happens must be recorded twice.

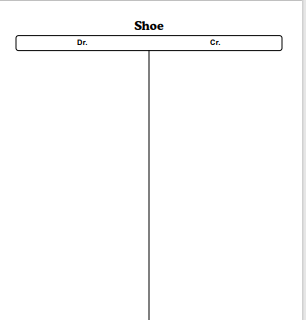

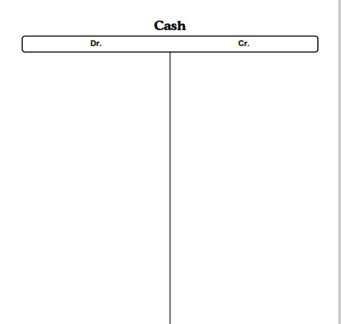

For example, if I sell a shoe for N20,000. The first effect is that I lost a shoe, and the second is that I gained N20,000 in cash. On my side, as the seller, I have lost the shoe and gained the money. As for the buyer, he has lost money and gained a shoe. This has a double effect on each of the parties.

Refer to the table below:

A double-entry report is done in an account.

An account is a page of a ledger that records transactions relating to a person or property. It’s always in a T-form, where the left-hand side is called the debit, and the right-hand side is the credit side. The title is written at the top.

Transactions on the other hand are monetary events in nature

We have two classifications of accounts.

1. Personal account

2. Impersonal account.

Personal accounts relate to persons: “both human beings and organizations”, debtors and creditors.

Impersonal accounts are accounts kept for properties. We have two subsets of Impersonal accounts: tangible properties and intangible properties.

Tangible account = Real account.

Intangible accounts = Nominal accounts.

Therefore, accounts are split into three main classes:

Personal accounts: (debtors and creditors) E.g. Philips account, Unilever Ltd account.

Real accounts are things we can see and touch (tangible) e.g. land, car, bike, cash, etc.

Nominal accounts: They are usually income and expenditure items. E.g. income, rent, salary, insurance, etc.

In my previous blog post, journal entry for beginners we used the DEALER approach as a guide to passing entries.

In this case, we will use the accounts for the same purpose. This is even better.

Personal account: Debit the receiver and credit the giver. E.g. you sell a good to Bayo, ask yourself, is Bayo receiving the goods or giving them? Since Bayo is receiving, you debit his account and vice versa if he is giving.

Real accounts: These are accounts of things we can see and touch. Like personal accounts, they cannot receive or give. The rule is to debit what comes in, and credit what goes out. As an example, when you buy a car, you debit, and vice versa.

Nominal account: debit all expenses and losses, credit income and gains.

P.S: We must always look at it from the point of view of the business.

The rules are effective for passing account entries.

#MEMBA11

Parenting and parenting styles

Parenting and parenting styles